The Simple Way to Send Money Abroad

Low fees, strong exchange rates, and no hidden costs.

Easy, fast, and secure international money transfers you can count on.

Easy, fast, and secure international money transfers you can count on.

Low fees. Great rates. No hidden costs.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Trusted by Millions

Billions Delivered Worldwide

Secure Transfers

Every transfer is protected by industry-leading security to keep your money safe.

Fast Delivery

Transfers typically arrive within minutes***, with real-time tracking from start to finish.

More Value

Strong exchange rates, low fees, and no hidden costs, so more money reaches your receiver.

Stay in Control

Track transfers, view history, and manage everything in one place with your Pangea Dashboard.

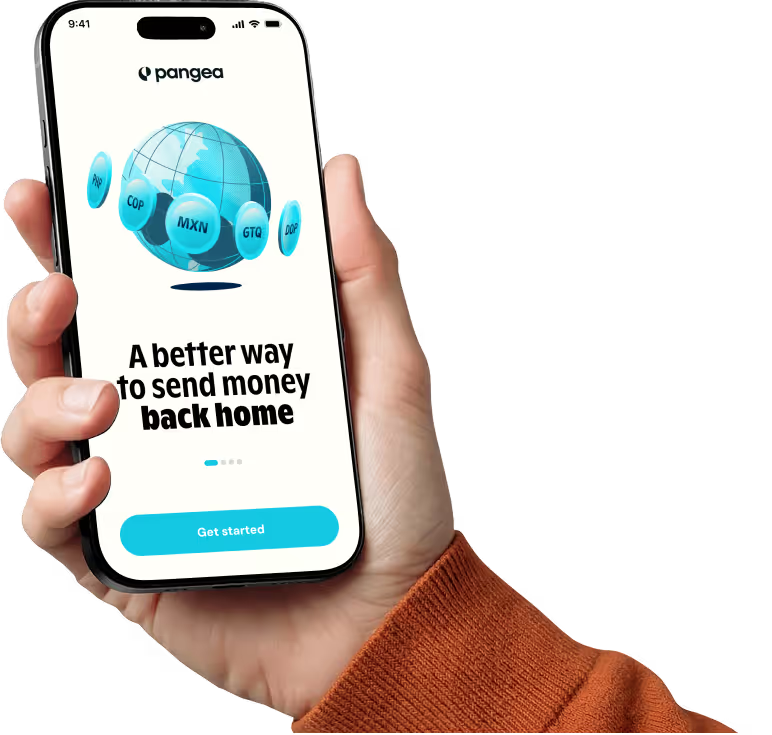

Download the

Pangea App

The international money transfer app built for low fees, strong rates, and real-time tracking, all right from your phone.

Send in Just a

Few Taps

Send money internationally in seconds with our easy-to-use platform. It's simple, seamless, and done right from your phone.

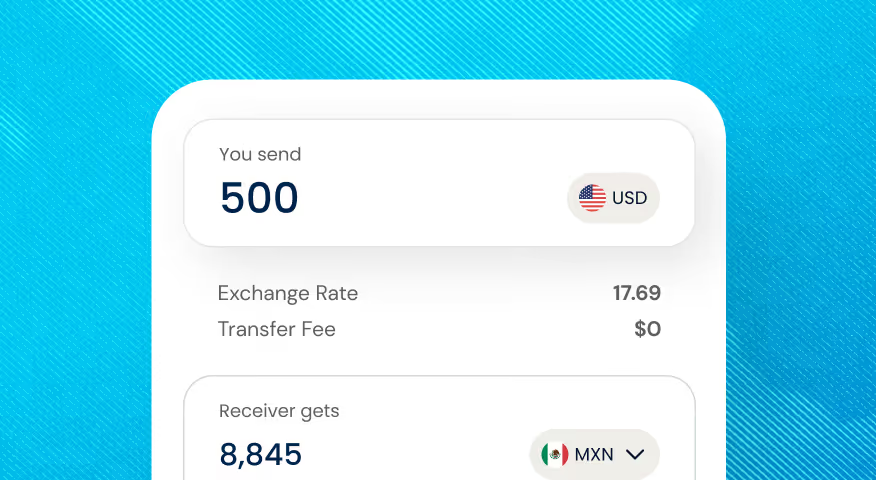

01. Enter Your Amount

See your exchange rate, fees, and how much your receiver will get.

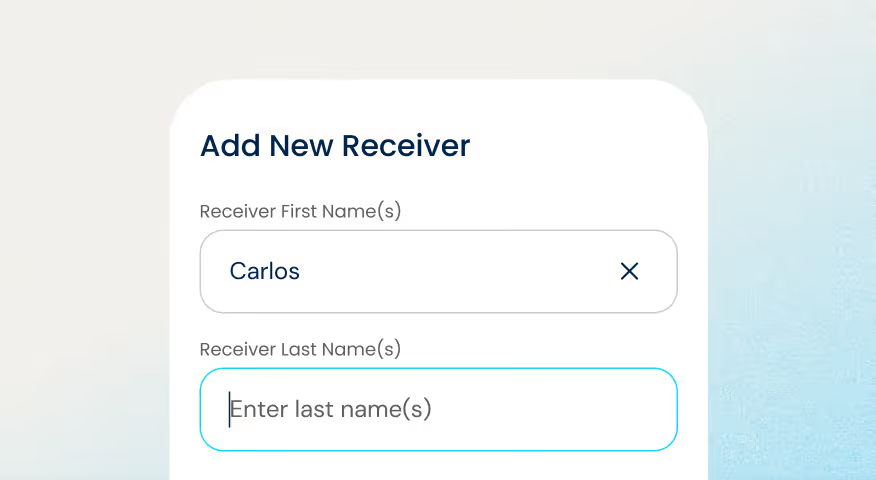

02. Add Your Receiver

Enter your receiver’s details, then choose their delivery method and how you'll pay for the transfer.

03. Send & Track

Confirm the details and send your transfer. Track it in real time.

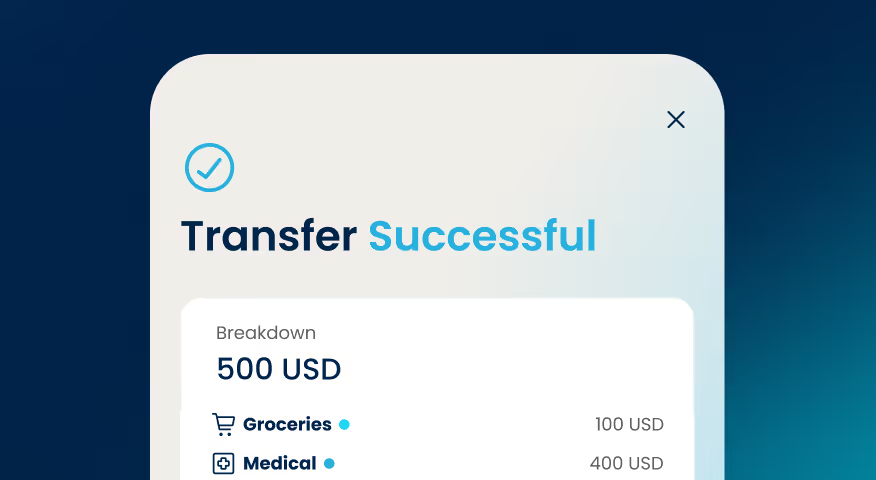

$100 USD sent

for Groceries

for Groceries

MXN 1,800

received by Mamá

received by Mamá

Get More From

Every Transfer

Every dollar matters. That's why Pangea combines low fees with strong exchange rates, so you get great value every time you send.

Manage All Your Transfers in

One Dashboard

Get a clear view of your transfers over time, all in one organized dashboard built to help you stay in control.

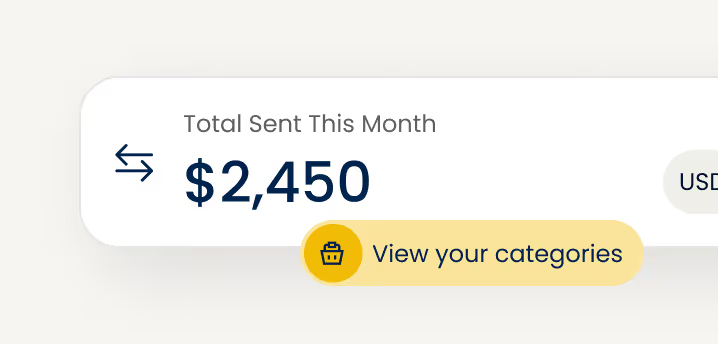

Stay on Top of Your Sending

Track monthly activity and understand your patterns at a glance.

See Everything in One Place

Transfers, totals, and receivers, all organized in a single view.

Plan Ahead with Confidence

Know where your money goes so you can budget and send smarter.

Secure. Licensed. Protected.

Your money and data are safeguarded with advanced security measures and strict regulatory standards, so you can send with confidence.

Real Stories from Real Customers

The easiest app to send funds with great exchange rates for Mexico. Highly recommended!

Iván

Verified Customer

Your process is fast, simple, and convenient. Thank you! Your service has been a huge help to my family 😊

Bianca

Verified Customer

This company implements security measures that effectively prevent any potential hacking of my account. The transfers are made very quickly. Also, Love the rates!

Dakila

Verified Customer

I just started using Pangea a few months ago, but it has been great, the money is transferred so fast, I don´t have to wait as with other transfer companies, and the best part is they offer a little more exchange for your dollars.

Vilma Salcedo

Verified Customer

I've sent money through other apps, but I didn't like that they even require you to provide a utility bill in your name. Pangea, on the other hand, makes sending money much easier.

Demi Recinos

Verified Customer

Frequently Asked Questions

How does Pangea protect my money and personal information?

How do I sign up for Pangea to send money from the U.S.?

What exchange rate will I get?

What transfer fees does Pangea charge?

Where can I send and receive money with Pangea?

How long does a transfer usually take to arrive?

What payment methods can I use for my transfer with Pangea?

How can my receiver get their money?

How much money can I send per transaction with Pangea?

Send Money to

Vietnam

Thailand

Senegal

Nepal

Uganda

Singapore

Kenya

Italy

Honduras

India

Indonesia

Malaysia

Germany

Ghana

Guatemala

El Salvador

Dominican Republic

Mexico

Colombia

Côte d'Ivoire

Burkina Faso

France

Bangladesh

Philippines

Send Money

Internationally to

24+ Countries

Ready to Send?

1 USD =

--

--

X

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.